On April 10, 2018, the Federal Reserve Board sought comment on a proposal to simplify capital rules for banks while preserving strong capital levels to maintain their ability to lend under stressful conditions. The proposal would reduce the amount of Tier-1 capital that large, medium and small-sized banks would need to hold as a buffer against future economic shocks – based on size, complexity, and systemic footprint of each firm. This should help small and mid-sized financial institutions and non-GSIB (Global Systemically Important Bank) banks free-up capital.

Additionally, lenders would no longer be required to set aside capital to pay dividends while they weather severe economic headwinds, and will see a dramatic reduction in paperwork while increasing transparency and ease-of-monitoring.

This proposal reflects the Trump administration’s desire to unwind regulatory excess in the financial sector and free-up capital for more productive use, while maintaining enough safeguards to prevent future banking crises.

Stress Testing Overview

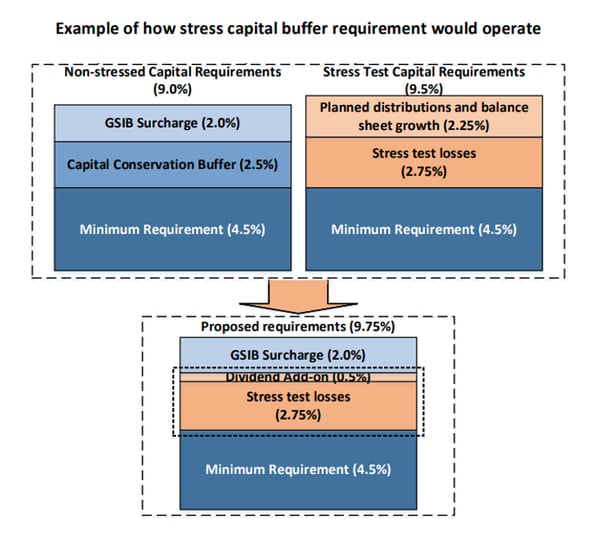

Stress testing assesses whether financial institutions have enough capital to a) survive adverse economic or financial conditions, and b) continue to make loans to creditworthy businesses and consumers. Its goal is to prevent a credit crunch through economic downturns and avoid a banking collapse. Stress testing, purportedly, makes the Federal Reserve Board’s (FRB) capital regime more forward-looking and risk-sensitive, but it comes at a huge cost to banks, with a disproportionate burden borne by small and medium financial institutions.

Under current regulations, financial institutions must conduct annual Stress Tests to determine the amount of capital they must hold to survive an economic shock and continue lending activity. While the concept of stress testing makes sense in the aftermath of the financial meltdown of 2007, the banking sector believes regulators went too far, and created rules that were too complex, too time consuming and too burdensome to implement, especially for small and mid-sized banks.

Proposed Changes

The Federal Reserve’s proposal would streamline existing rules to:

- Simplify the FRB’s capital regime by combining the quantitative assessment of capital analysis with buffer requirements in the Board’s regulatory capital rule, and

- Reduce the compliance burden for smaller, less complex firms subject to the supervisory stress test.

Net Impact

Net Impact