According to the Federal Reserve Bank of San Francisco, cash is still the most frequently used retail payment instrument; used in nearly one-third of all transactions, even when other options are available. Data also shows that 89 percent of all Americans carry cash to some extent, and nearly two-thirds hold cash every day. As a result, consumers are dependent on banks and credit unions to get the cash they need for everyday spending. However, branches and ATMs do not always meet their demand for cash. Such shortfalls damage customer confidence and are the result of three branch cash management mistakes that most banks and credit unions do not even know they’re making but can easily rectify.

From first-hand experience, banking executives acknowledge that customer demand for cash follows in distinct recurring patterns, year after year. However, their assumptions about the timing and magnitude of these cash cycles often do not match actual demand and usage patterns.

For instance, banks and credit unions expect, and plan for a significant increase in cash demand during the Christmas holiday season. But, in reality, only about 40 percent of all financial institutions actually experience an increase in cash demand during this time. Instead, banks and credit unions see increased demand for certain denominations, typically $1s and $100s that people like to use for cash gifts. On the flip side, branches sometimes see a corresponding decrease in demand for $10s, $20s and $50s during the holidays. As a result, the branch’s aggregate demand for cash does not change all that much; what often changes is relative demand for different denominations.

Banks and credit unions often boost cash levels in anticipation of the holiday season, which results in excessively high cash inventory levels. The entire branch network following this mistake causes a large stock pile of idle cash for the organization. Consequently, depending on how quickly a branch returns to normal cash levels, this idle cash remains a non-earning asset and hurts the FI’s profits if it isn’t invested to generate returns.

Seasonality - Cash Demand Rises in February and March

In working with hundreds of banks and credit unions, cash demand rises in February and the beginning of March when tax refunds start coming in for those who expected to get money back and filed their taxes early. Additionally, refunds are typically cashed at ATMs, so demand for $20s goes up.

The seasonality of cash demand is also affected by customer demographics at the branch location. For example, branches in neighborhoods with young school-going children see a spike in demand at the beginning of the school year and when summer vacations start. And branches in, say, rural farm areas might see higher cash demand when harvesting season begins.

Branches must, therefore, accurately study local cash demand patterns and adjust their cash availability and denominations to match these trends.

Some banks and credit unions assume that cash demand stays flat year-over-year. Such an assumption may be valid in a region that sees no growth in its customer base or in the local economy, but would fall flat where there is demographic and economic growth. For instance, if a branch’s customer base grows by just 10 percent in a year, the branch and the ATMs in the area will see a meaningful increase in cash demand and should be prepared to satisfy it.

Fallacy of Assuming Cash Demand Stays Flat Year-Over-Year

Here’s a real-life case study of a $990 million credit union in a region that experienced strong economic growth: Within a year, the credit union saw a 17 percent increase in cash usage, a 20 percent rise in the use of $50s and a 69 percent jump in the use of $100s. Had this credit union set its cash limit to be the same as last year’s amount, it would not have been prepared for the significant increase in demand for cash and specific denominations. This example proves that FIs must not get trapped in the fallacy of holding cash levels steady year-over-year, but should proactively adjust cash levels to meet growth and seasonal trends.

Oftentimes, branch cash managers use their experience, tenure or gut feelings to intuitively manage cash inventory and denomination levels, and count the frequent placing of non-routine cash orders as business as usual. This approach inherently leads to denomination outages (more frequently than the branch would like) that annoy customers, increase cash delivery costs, and cause excessive cash levels that represent a missed opportunity to increase branch profits through loans and other investments.

Leverage branch cash management Solutions

Instead, banks and credit unions should manage cash no differently from managing any other type of inventory - by installing a sophisticated branch cash management system.

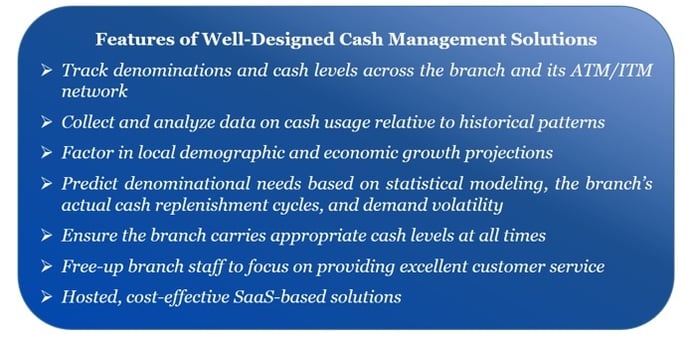

Such systems track denominations and cash levels across the branch and its ATM/ITM network, collect and analyze data on cash usage relative to historical patterns, factor in local demographic and economic growth projections, and predict denominational needs based on statistical modeling, the branch’s actual cash replenishment cycles, and demand volatility.

Well-designed cash management solutions prevent branches from making common mistakes, ensure appropriate cash levels at all times, reduce branch operating expenses, and free-up branch staff to focus on providing excellent customer service and pursuing profitable business development activities, such as making new loans.

Sources:

https://www.frbsf.org/cash/publications/fed-notes/2017/june/cash-holdings-new-view-on-cash

http://www.cunacouncils.org/news/7108/news-article/

http://www.cutoday.info/THE-tude/4-Myths-Around-Cash-Management