Depository institutions, such as banks and credit unions, can significantly reduce their reserve requirements and eliminate balances held at the Federal Reserve Bank by implementing retail sweep (aka Deposit Reclassification) programs. Freed-up balances can then be used to boost lending and increase profits. It is best for depository institutions to implement a tried and true retail sweep solution because their sweep percentages optimize non-reservable balances and maximize earnings potential.

A Brief Overview of Reserve Requirements

The Federal Reserve imposes reserve requirements on depository institutions – such as commercial banks, savings banks, savings and loan associations, credit unions, and U.S. branches of foreign banks - so they have sufficient cash on hand to meet day-to-day transactions and accommodate unexpected large withdrawal requests, within reasonable limits.

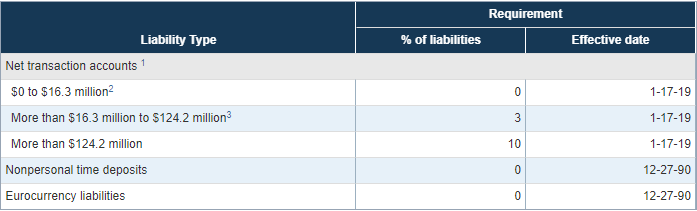

The required reserve depends on the size of the deposits the financial institution (FI) holds - as determined by the dollar-amount of net transaction accounts.

A transaction account (such as a checking account, current account or demand deposit account) is a deposit account held at a bank or other financial institution, with funds available to the account owner "on demand" for frequent and immediate access either through cash withdrawals, checks or electronic transfers. In economic terms, the funds held in a transaction account are regarded as liquid funds and in accounting terms they are considered equivalent to cash.

Net transaction accounts, simply put, represent the difference between the bank’s liabilities (the sum total of demand deposit and equivalent accounts, and the bank’s obligations maturing in seven days or less such as maturing certificates of deposit) and its assets coming due soon (such as amounts imminently due from other depository institutions and cash that is in the process of collection).

As of 2018, the Federal Reserve exempted FIs with net transaction accounts of $0 - $16.3 million, and imposed reserve requirements of 3 percent (reserve ratio) of liabilities for net transaction accounts of $16.3 million to $124.2 million (“the low reserve tranche”) and 10 percent for net transaction accounts of over $124.2 million, per the table below.

Source: https://www.federalreserve.gov/monetarypolicy/reservereq.htm

Depository institutions that have at least $16.3 million in net transaction accounts have to submit form FR 2900 to the Federal Reserve on a weekly basis. The form asks for information on transaction accounts, time and savings deposits, vault cash, and other reservable obligations; the Fed then uses this data to calculate required reserves.

Reserve requirements must then be met through any combination of vault cash and deposits maintained either with a Federal Reserve Bank or with another institution in a pass-through relationship (“the Fed balance”). The vault cash component of reserves earns no interest but, through a 2008 authorization by Congress, all required and excess reserves held at the Fed receive interest, typically equal to Fed Funds rate (2 percent as of August 2018).

Retail Sweep Programs Reduce Reserve Requirements and Eliminate Fed Balances

In a “retail sweep program,” a depository institution creates two accounts (sub-accounts), a savings and checking, for each transaction account. Transfers of funds occur between a customer’s transaction sub-account (subject to reserve requirements) and that customer’s savings sub-accounts (not subject to reserve requirements) by means of preauthorized or automatic transfers to cover the customer’s transaction activity. As a result, a retail sweep program reduces transaction account reserve requirements while providing the customer full access to funds.

The Fed has three key criteria for retail sweep programs to comply with Regulation D (Reserve Requirements of Depository Institutions):

- a depository institution must establish, by agreement with its transaction account customer, two legally separate accounts - a transaction account (a NOW account or demand deposit account) and a non-transaction account (usually a savings deposit account, also called a “money market deposit account” or “MMDA”);

- the swept funds must be moved from the transaction account to the savings deposit account on official books and records as of close-of-business on the day the depository institution intends to report form FR 2900; and

- the maximum number of preauthorized or automatic funds transfers (“sweeps”) is limited to six per month (to accommodate weekly FR 2900 submissions).

Curious to know your exact benefits from Deposit Reclassification?

Deposit Reclassification Significantly Improves and Maximizes Sweep Percentages

If implemented correctly, Deposit Reclassification can sizably reduce a depository institution’s reserve requirements – to the point where it meets its obligations with vault cash alone and does not have to park funds at the Fed.

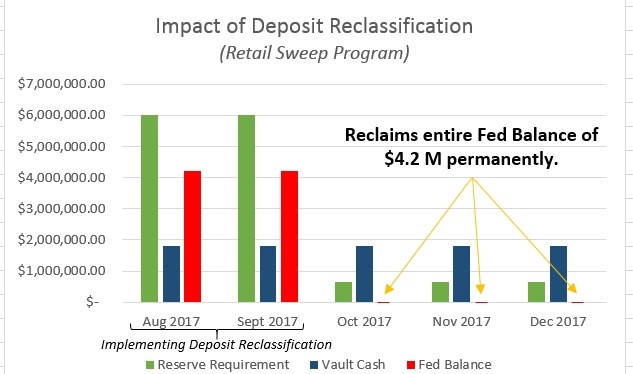

Here’s a simplified example to show the impact of Deposit Reclassification. Before Deposit Reclassification, the dollar-amount of ABC Institution’s net transaction accounts resulted in a reserve requirement of about $6 million, which the FI met with $1.8 million in vault cash and $4.2 million deposited with the Federal Reserve Bank (the Fed balance). Then, after the institution implemented a retail sweep program, its reserve requirement dropped almost 90 percent to $650,000, which it more than met with its vault cash of $1.8 million. As a result, the FI eliminated its Fed balance of $4.2 million.

Source: logicpath

So Deposit Reclassification can eliminate Fed balances, and give banks and credit unions the opportunity to reinvest these freed-up monies in their communities as business loans, home loans, car loans, community development loans, etc. Moreover, these loans earn higher rates of interest than the Fed Funds rate that the bank or credit union would have received on its Fed balance, so retail sweep programs are key to boosting a depository institution’s profits, with the added benefit of investing in communities and generating goodwill.

However, Deposit Reclassification cannot be done only at the general ledger or on the books. Depository institutions must create sub-accounts at the account level and are best served by implementing a Deposit Reclassification solution that maximizes sweep percentages by reclassifying as much as 60-80 percent of all transaction accounts into savings deposit accounts. Deposit Reclassification is initiated after receiving approval from the local Federal Reserve Bank, and typically takes 30-45 days to receive a response. During this time, the FI can implement and have Deposit Reclassification fully up and running, with about 4-6 hours of bank staff time. With a Deposit Reclassification solution, banks and credit unions can recover their Fed balances, invest in their communities, and increase their earning assets and profits – all without searching for new deposits or impacting their customers.

Curious to know how other banks and credit unions reclaimed their Fed balance?

Read their Case Studies

| United Federal Credit Union | Venture Bank |

| Traditions Capital Bank | Richfield-Bloomington Credit Union |

| Biddeford Savings Bank | |